EngineeringRobo’s Cryptocurrency / Stock Tax Guide

In this guide, you will learn everything you need to know about bitcoin and cryptocurrency taxation in Canada.

If you’ve bought and sold cryptocurrency in the last calendar year, it’s time to start thinking about the impact this may have on your income tax return. Whether you’ve made a profit or a loss trading cryptocurrency, you’ll need to declare it in your annual tax return.

In Canada, cryptocurrency is generally treated as a commodity, which means it is taxed as either income or a capital gain. It’s essential that you understand the tax consequences of your specific situation when it comes to buying, selling and trading crypto. In this guide, we look at the basics of cryptocurrency tax in Canada to help you learn what you need to do to keep the taxman happy.

It’s almost everyone's favourite time of the year! Tax season is getting closer! EngineeringRobo Team get a lot of questions about how cryptocurrency gains or losses are taxed, and we’ve published this updated 2020 tax guide to help you out.

Before we dig into the weeds of capital gains in Canada, there's something you should know. This is general information on capital gains to give you a better understanding of how it works. Since everyone's situation is unique, this should not be taken as advice and you should always consult a tax professional to determine what works best in your specific situation.

Crypto taxation in Canada

The Canadian Senate reviewed the issue of taxation of cryptocurrency already in 2014 to address the growing popularity. The Canadian Revenue Agency (CRA) has published guidance to help Canadians understand the tax implications of cryptocurrencies better.

The CRA considers bitcoin and other cryptocurrencies to be a commodity with regards to taxation. In general, each disposal of a crypto is a taxable event:

⚫️ Selling of cryptocurrency and you receive fiat currency (such as Canadian dollars)

⚫️ If you trade or exchange cryptocurrency (includes also crypto-to-crypto transactions)

⚫️ Gifting cryptocurrency to another person

⚫️ Use cryptocurrency to pay for goods or services

How is cryptocurrency taxed?

The profit made from cryptocurrency is determined in Canadian dollars when you exchange cryptocurrency for fiat or cryptocurrency, or you use it for goods and services.

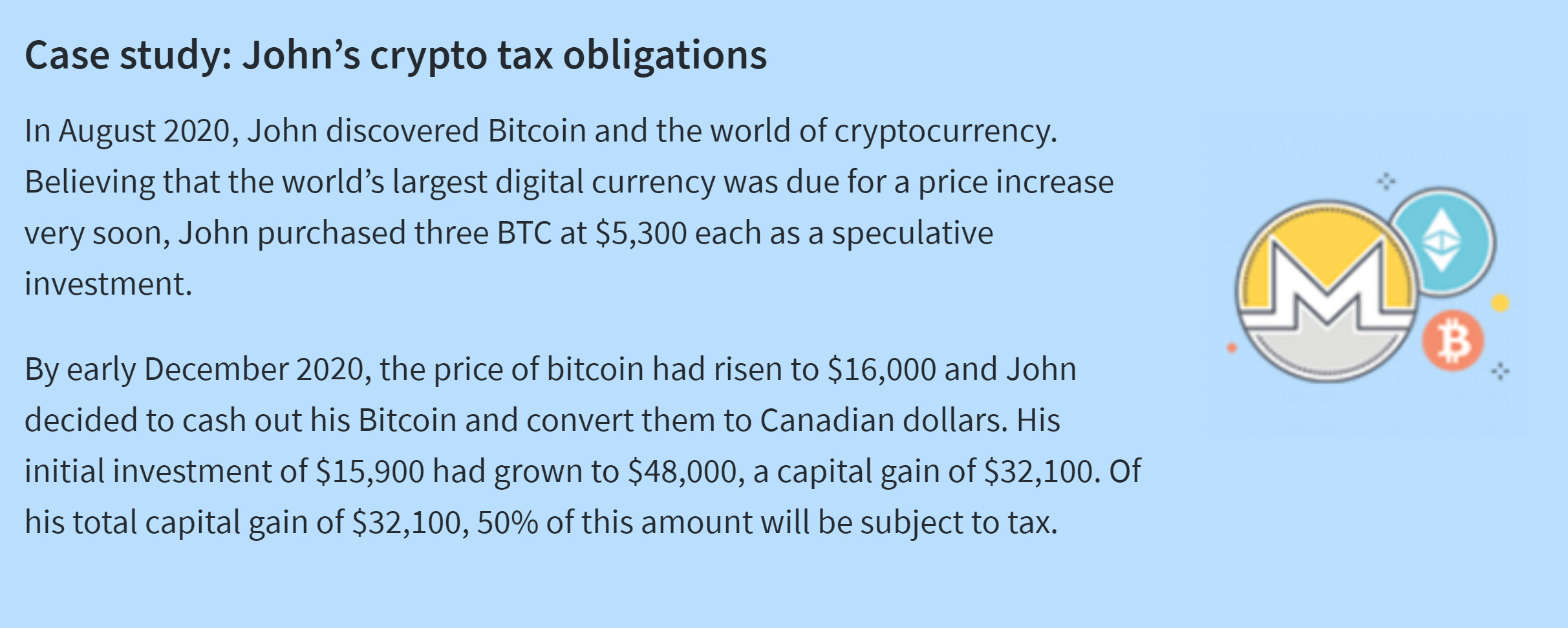

For example if you buy or otherwise obtain 1 BTC when it’s worth $5,000, and then sell or spend it all when it’s worth $13,000, you’ve made a capital gain of $8,000. Capital gains have a tax obligation of 50%, meaning you’d have to pay tax on 50% of the gain.

Income from cryptocurrency transactions is either treated as business income or as capital gains. Business income is treated differently for tax purposes than capital gains.

John regularly buys and sells various types of cryptocurrencies. He pays close attention to the fluctuations in the value of cryptocurrencies and intends to profit from the fluctuations. His activities are consistent with someone who is engaged in the business of day trading.

In 2019, John sold $150,000 worth of various cryptocurrencies, which he originally purchased for $40,000. His net profit is $110,000.

Since John is actively trading in cryptocurrency, which is a commercial activity, he reports business income of $110,000 on his 2019 income tax return.

Kieran found a deal on a living room set at an online vendor that accepts Bitcoin. Kieran acquired $5,500 worth of Bitcoin to buy the furniture with. By the time he bought the furniture and converted his remaining Bitcoin back into dollars, the value of Kieran ’s Bitcoin had increased by $2000.

The gain realized by Kieran was on account of capital, so Kieran has to report a $2000 capital gain on his income tax return. However, only 50% of that capital gain is taxable.

On September 26, 2020, Marcus bought 100 units of Ethereum, which had a value of $20,600. For this purchase, Marcus used 2.5061 Bitcoins, which were trading at $8,220 per unit on that day, or the equivalent of $20,600. We consider that Marcus disposed of those Bitcoins.

Marcus originally bought those Bitcoins for $15,000 and exchanged them for 100 units of Ethereum at a value of $20,600, resulting in a capital gain. It is calculated as follows:

$20,600 [fair market value of 2.5061 Bitcoins at the time of transaction]

- $15,000 [adjusted cost base of 2.5061 Bitcoins, their original purchase price]

$5,600 capital gain

$5,600 capital gain taxed at 50% = $2,800 taxable capital gain

If the original purchase price of the 2.5061 Bitcoins had originally been $25,000, but at the time that Marcus exchanged them for 100 units of Ethereum they were worth only $20,600, he would have a capital loss. It is calculated as follows:

$20,600 [fair market value of 2.5061 Bitcoins at the time of transaction]

- $25,000 [adjusted cost base of 2.5061 Bitcoins, their original purchase price]

$4,400 capital loss

$4,400 capital loss × 50% = $2,200 allowable capital loss

This example assumes that the cryptocurrency in question was held as an investment on account of capital; however, if this transaction occurred in the course of conducting a business, the entire amount of $5,600 would need to be reported as income in the first transaction and the entire $4,400 would be reported as a loss in the second transaction.

Tax on Income from Mining / Staking / Air Drops / Hard Forks / ICOs

Mining of cryptocurrency

The bitcoin blockchain is secured by what we refer to as miners. By using specialized hardware to solve complex mathematical equations, miners make it possible for me and you to transfer bitcoin and trust that it will be sent to the rightful recipient without the use of third party service. To incentivize miners to do this (also called Proof-of-Work), they are rewarded with newly created bitcoins and also the fees paid for each transaction.

Cryptocurrency received as payment for mining is subject to tax treatment in almost all countries, with Canada being no exception. Again, the tax treatment depends on whether your mining activity is classified as a business or just a hobby. If you are mining crypto such as bitcoin or ethereum with the intention of making profits on a regular basis, you will most likely be considered conducting business activity and the crypto received will be taxed as business income.

You can normally deduct any directly associated costs like electricity and computer hardware from your mining income. You should also be aware that when you decide to sell the coins later, the sales proceeds will become part of your business income and taxed as such.

If your mining is just a personal hobby, you will only pay capital gains tax when you later sell (dispose of) the received coins. Because you didn’t pay anything for the coins originally, the cost basis should be considered as zero so that your capital gains are equal to the market value (in CAD) at the time when you sell the coins in the future.

The CRA says that it will be decided case by case if your activity is classified as a business or just a hobby.

Staking of cryptocurrency

The Canadian Revenue Agency has not released specific guidance for staking of cryptocurrency. Because staking is similar in nature to mining of cryptocurrencies, the safest approach is to treat received coins from staking in a similar fashion to mining.

Airdrops

Airdrop of cryptocurrency tokens is often done as part of a marketing or advertising campaign. In some cases, you will need to register before a deadline to become eligible to receive tokens. You may also receive tokens just from holding another cryptocurrency in your wallet or on an exchange.

The CRA has not issued specific guidance to the tax treatment of cryptocurrency airdrops, but a safe approach is to pay capital gains tax when you later decide to sell the coins. Similar to crypto received from mining, you should assume a cost basis equal to zero because you did not pay anything to acquire the coins.

Hard Forks

Blockchains, e.g. the bitcoin blockchain, need to be updated from time to time. Such updates can result in a soft fork or hard fork. Updates that automatically get adopted by all participants is called a soft fork. This does not result in the creation of new tokens or a new blockchain. A hard fork, on the other hand, can result in a blockchain split where new tokens come into existence.

The Canadian Revenue Agency has not provided specific guidance for how cryptocurrency received from hard forks should be treated for tax purposes. Again, a safe approach is to pay capital gains tax when you later decide to sell the coins and assume a cost basis equal to zero similar to airdrops explained above.

ICOs & IEOs

ICOs (“Initial Coin Offerings”) and IEOs (“Initial Exchange Offerings”) are a popular form of raising capital by companies and projects launching their own blockchain or token. In both cases, a person typically invests in a token that will be released in the future and pays with another cryptocurrency like bitcoin or ethereum.

The Canadian Revenue Agency has not provided specific guidance for the treatment of ICOs or IEOs, but since this is very similar to a crypto-to-crypto transaction, we can treat such transactions similarly for tax purposes. If you invest in token XYZ and pay with bitcoin, you will have to calculate capital gains on the bitcoin disposed of. You will need to use the fair market value of bitcoin on the date you made the investment which will also become the cost basis for the newly purchased tokens.

Taxes on Buying / Selling / Trading cryptocurrency

Taxation of Foreign Crypto

Cryptocurrencies that are situated, deposited or held outside of Canada are also subject to reporting requirements for Canadian tax purposes. Indeed, since Canadians are taxed on their worldwide income, not just their funds in Canada, even if the cryptocurrency platform you use is foreign, you are still obligated to report the realization of any profits when you trade. Accordingly, Canadian taxpayers holding cryptocurrency outside of Canada that has at any time exceeded $100,000 CAD within the year should be aware of their obligation to file Form T1135 to report the property.

What if my cryptocurrency is lost or stolen?

If you lose your private key or your crypto holdings are stolen, you may be able to claim a capital loss. However, whether or not this is possible may depend on whether you lost the cryptocurrency, lost evidence of your cryptocurrency ownership or you lost a private key that cannot be replaced.

If an item can be replaced, it is not considered to be lost. But a lost private key is irreplaceable, so it may be possible to claim a capital loss by providing detailed evidence, including:

⚫️ The dates when you acquired and lost the private key.

⚫️ The public wallet address linked to the private key.

⚫️ The total cost of acquiring the cryptocurrency that was later lost or stolen.

⚫️ The cryptocurrency wallet balance when you lost the private key.

⚫️ Proof that you actually owned the wallet (for example, transactions linked to your identity).

⚫️ Possession of the hardware where the wallet is stored.

⚫️ Transfers to the wallet from a digital currency exchange where you hold a verified account, or where your account is linked to your identity in some other way.

It is not clear today how the CRA treats lost or stolen cryptocurrency. However, most countries allow the taxpayer to deduct the original cost from their capital gains if they have been a victim of fraudulent actions or permanently lost access to their private keys.We recommend that you ask a certified tax professional in Canada if this applies to you.

Will the CRA investigate my transactions?

Under sections 231.1 to 231.4 of the Income Tax Act the CRA has broad powers to investigate and demand information from taxpayers. Although this investigative power is not absolute, the actions of the American Internal Revenue Service (IRS) may foreshadow what is to come for Canadian taxpayers.

In November 2017 the success of a court order brought by the IRS, forced Coinbase, an American cryptocurrency exchange to turn over information on its users. The petition by the IRS had been instigated on the basis that Coinbase advertised that its platform served 5.9 million customers through more than $6 billion in transactions, despite only 800-900 taxpayers reporting gains related to crypto from 2013 – 2015.

Canadian tax authorities may similarly require online exchanges to provide documentation on its users if it believes compliance with tax regulations is not sufficient.

In November 2017 the success of a court order brought by the IRS, forced Coinbase, an American cryptocurrency exchange to turn over information on its users. The petition by the IRS had been instigated on the basis that Coinbase advertised that its platform served 5.9 million customers through more than $6 billion in transactions, despite only 800-900 taxpayers reporting gains related to crypto from 2013 – 2015.

Canadian tax authorities may similarly require online exchanges to provide documentation on its users if it believes compliance with tax regulations is not sufficient.

Canadian tax authorities may similarly require online exchanges to provide documentation on its users if it believes compliance with tax regulations is not sufficient.